Español

Español Deutsch

Deutsch Ελληνικά

Ελληνικά Italiano

Italiano Polski

Polski Română

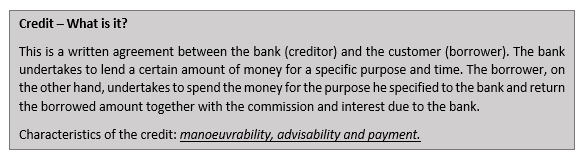

RomânăCredit

Contents

Source: https://www.pexels.com/photo/abundance-bank-banking-banknotes-259027/

Loans:

There are different types of loans that are offered by banks, but also by other financial service providers. They differ in terms of amount, maturity and conditions. They may be repaid in full, as a lump sum or instalments.

Credit cards:

When you apply for a credit card, you are given some specific amount of money for your disposal. The amount depends on several factors, in many countries (e.g. USA, UK, Germany) so-called credit score is used, in others you are required to provide documents proving your monthly income, place of work, etc.

Source: https://pixabay.com/pl/photos/karta-kredytowa-master-card-1520400/

The credit must balance itself once a month – meaning that you purchase goods over a month, but eventually you will need to pay it off. Failure to pay typically results in interest rates and late fees. However, being on time with payments, usually helps to build positive credit history, which is often needed when trying to get a bigger loan, like for buying a house.

There are many companies issuing credit cards, most known are probably Visa, MasterCard, American Express, Dinners Club, Chase and so on.

Very often the cards are branded – either by your own bank or other companies, not necessarily financial, e.g. Amazon offers their own cards, most bigger airlines, shopping chains, etc. Normally that means that besides issuer logo – e.g. Visa, the card also has a logo of your bank or shopping chain, airline, etc.

Typically, there is an annual fee – which varies a lot and could be none if you fulfil specific conditions, like minimum amount spent yearly or monthly.

It is worth noting that credit cards interest rates are often very high – but can be avoided completely when paid on time.

Installment credit:

It can be repaid in a certain number of instalments. This is a simple payment program. This plan is used to buy various items, e.g: furniture, cars. An advance payment is initially required. The remainder shall be paid by a certain number of equal instalments. According to the agreement, the purchased item is a security or pledge for the debt. Examples: home equity loans, home mortgage, automobile loan, home improvement loan.

Revolving credit:

This loan consists in increasing the account balance by an additional amount, which the customer can use as he wants and whenever he wants.

Source: https://www.pexels.com/photo/bank-banking-banknotes-business-210574/

The cost of the credit

The credit price is influenced by many factors:

- the amount of market interest rates and the cost of required reserves (which are determined by the central bank),

- credit risk level (determined by the bank),

- amount of credit,

- the length of the period for which the loan was granted (the longer the time, the higher the interest),

- the interest repayment frequency,

- costs incurred by the bank,

- method of calculating interest (simple interest or compound interest)

The cost of credit is also influenced by the interest rate: variable (where the interest rate depends on the current market situation: during a worse economic situation we will pay less and during a good economic situation our installment will increase) and fixed (which guarantees a stable burden on the household budget, but over 20-30 years may also cause losses). Banks are very reluctant to grant loans at a fixed interest rate during a worse economic situation.

When taking a credit, you decide on the type of interest and capital installments (degressive or fixed).

In the case of decreasing loan instalments, the capital installment are equal to the capital (obtained by dividing the amount of credit granted by the number of installments specified by the customer) and decreasing interest, which is charged on the current amount of debt.

With fixed instalments (at the same level over the whole period), the interest rate decreases and the capital installment increases.