Español

Español Deutsch

Deutsch Ελληνικά

Ελληνικά Italiano

Italiano Polski

Polski Română

RomânăFinancial independence

Contents

As in many other sectors of life, for complex processes, it is useful to develop a plan. You can imagine a big family event, per example a wedding with 130 participants, without a detailed plan, made very early, before the event and followed by the whole team involved in the process. Even with the best plan, during the implementation several non-predictable aspects will require immediate interventions and corrections. But during these crisis situations, the plan itself is the main reference point, with its main aims, which can guide us to make the most appropriate corrections, without loosing the most important objectives!

This is very similar also for our FINANCIAL PLAN, aiming at to reach financial independence, while making the best choice in difficult moments.

Of course, the financial independence has a cost, and we need to navigate between rights and obligations, with a sound knowledge of them and respecting the rules of the play. Here are the main steps of the process;

A. Where I am today?

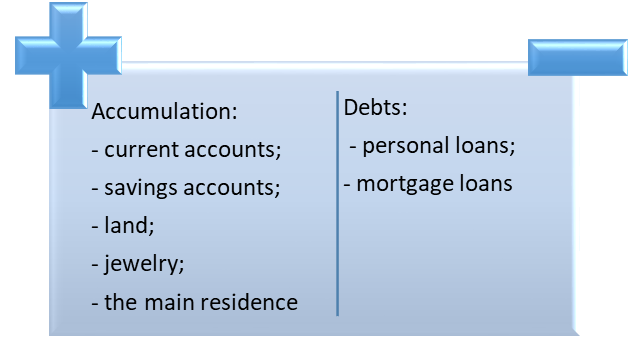

This is the inventory for the current situation, which need to be very concrete and real. Basically this is a balance of our ACCUMULATIONS & DEBTS.

The net worth can be INCREASED by adding more units to the ACCUMULATION and/or decreasing the DEBTS.

The cash flow analysis is the balance between the expenses and incomes, and a negative balance is one of the most serious stress factor in our life!

Thomas Jefferson advice us to “Never spend your money before you have earned it.”, expressing the essence of the positive cash flow.

The main questions need to be answered by the cash flow analysis are the following:

- Where I am spending more than needed: that I can afford? Frank A. Clark opinion is that “Many folks think they aren’t good at earning money, when what they don’t know is how to use it.” It is essential to very attentively analyse the spending, and to accept that there are possibilities to learn how to improve our habits of spending! The cash flow analysis will offer you an easy instrument to find the main possibilities to control your spending. This does not mean to simply renounce to all the pleasure, but will support you to better control the When? & How?, thus decreasing the expenses, but in the same time covering the personal needs.

- I am investing money for the future of my family? This is one of the most difficult tasks, when discussing about investments, in the very far future, and even in others future, not only mine! Like Robert Kiyosaki express this idea, “It’s not how much money you make, but how much money you keep, how hard it works for you, and how many generations you keep it for.” For this we really need to exercise the decisions between answering the most urgent need or investing in some future, even unknown needs of mine or my family members. We are very often making big confusions between URGENT need and IMPORTANT needs. Because of the apparently urgent character of a need, we are likely to consider that they are also important, and we act under the pressure of urgency, instead of ignoring the intervention of the results maybe is not as important as urgent seems to be. This confused reaction of us is staying behind the „SAVE advertising„, You save 0,111 cent if you buy NOW that product, „Limited stock„, and we immediately are buying that product, under the pressure of urgent action, and with the false promise of SAVING, Instead, very often we buy goods we don’t really need them. This is not saving, this is not even urgent, not for us; but it was urgent for the company.

- It is the time to save some money? “A simple fact that is hard to learn is that the time to save money is when you have some.” —Joe Moore, and sometimes is difficult to respect the financial discipline, and save a certain amount of money always, when we register some incomes. It is a source of pleasure to immediate spend money when they entered our accounts, and we are pushed to forget the savings, because these are only a promise for some pleasure but not in this moment, only somewhere in the future. If the savings are dedicated for a very far objective, it is even more difficult to respect the saving promises.

- Spend or save? The answer is very easy by Dave Ramsey: “You must gain control over your money or the lack of it will forever control you.” This is the essence of the cash flow tool, providing you the most important tool towards the financial independence. The correct question is not the Spend OR save! Of course we will spend AND save! And the only small details is in the balance between them!

- Small money does not matter! This is another miss-belief of us, and for this is enough to check your payment invoice, at the supermarket, when buying only small items, only with reduce prices, and at the end of the list of small prices, is a total of three numbers. Just take into consideration a coffee to go, selling a cup of coffee for less then 1 euro, which is considered not too much, in comparison with a coffee shop in the downtown, where you pay 7-9 euro for a coffee. But our coffee to go owner knows very well that he will make a good revenue, if he sell a greater amount of coffee!

We start to make the inventories, and carefully analyse each item, to check id the INCOME items could be increased, and the EXPENSES items are possible to be decreased.

For the incomes you can consider:

For the expenses you can consider: